Every penny counts towards your retirement and it’s vital to sock away as much as you can afford, especially while you are young. How much can you afford to invest? Let’s assume you can invest $300 each month ($3,600 each year).

Every penny counts towards your retirement and it’s vital to sock away as much as you can afford, especially while you are young. How much can you afford to invest? Let’s assume you can invest $300 each month ($3,600 each year).

Every time you look at your investments it appears to be growing; albeit slowly. Is there a way to kick-start your investment account? There is, but it’s going to require an entirely different mindset about what risk truly is and an understanding of how risk can be managed. Let’s discuss…

Most homeowners have equity in their house and each and every month as the mortgage is paid down this equity continues to grow. Unfortunately this equity earns $0. Of course the value of your home appreciates slowly over time, but this would happen regardless of what you owe on it.

Your home equity can be accessible to you by obtaining a home equity line of credit. Banks assess the value of your home and will provide you with a line of credit of 65-80% of its value less your mortgage balance(s). Here’s how it works:

- House value: $308,000

- 65% of value = $200,200

- Mortgage balance(s): $100,000

In the above scenario the bank will offer you a home equity line of credit for $100,200 ($200,200 minus $100,000). Boom! You have access to $100,200 that you can spend however you wish. But… be very careful! Many people rush out and spend these funds on new kitchens, bathrooms, pools and the list goes on. It’s vital to remember that you will be paying interest on every dollar you spend until you pay it off. In this instance I pay 3.20% / year (which is my bank’s prime rate + 0.50%) so if I were to spend all $100,000 I would be paying $3,200 / year or ~$267 / month in interest. This is less than the $300 each month that you can afford, except you would have $100,000 in the market from the get go instead of building slowly up to that over the next 10-20+ years.

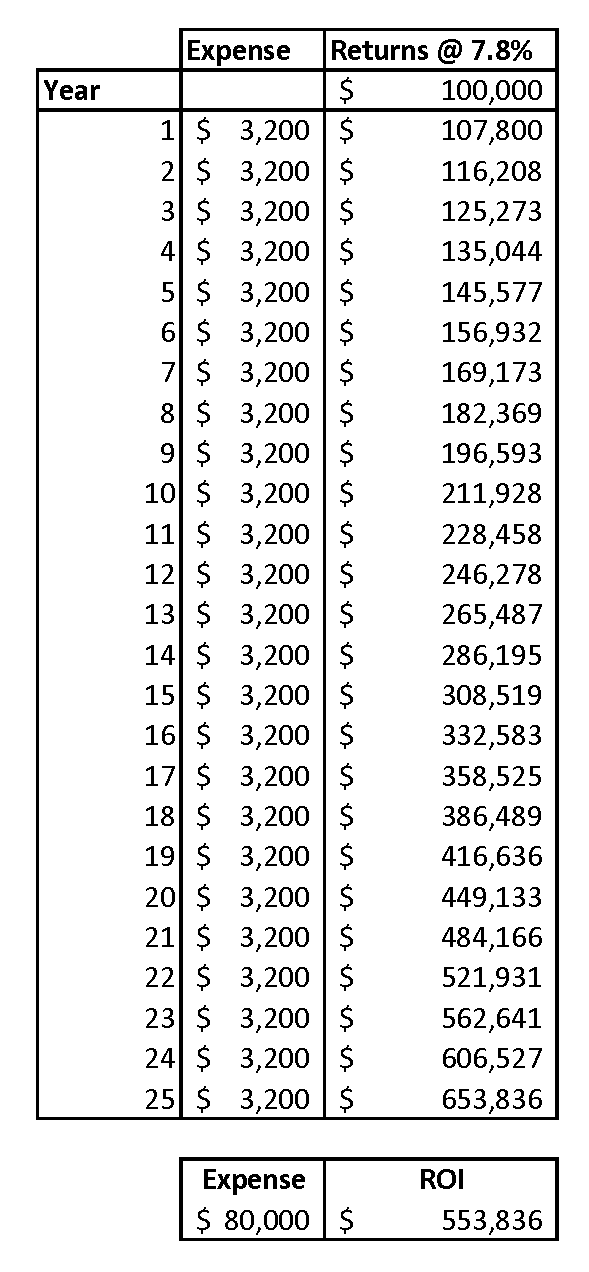

There are huge advantages to this, while you’re only paying $3,200 / year in interest, you are likely to earn much more based upon the fact that the stock market has averaged a return of 10.1% (7.8% adjusted for inflation) over the last 50 years. Furthermore because your returns will compound each and every year, you are likely to to double your investment every 7-9 years. Oh and the cherry on top? Since you invested those funds in the stock market with a reasonable expectation of returns, each year on your income tax you are entitled to legally write off the $3,200 as an investment expense (please talk to your accountant for all of the do’s and don’ts to ensure this is done legally). Not only are you earning returns from your home equity that would otherwise sit idle, you’re also lowering your taxable income burden at the same time! Bam!

Over the duration of 25 years, in this scenario, you will pay $80,000 in expenses (which you can write off on your income taxes) and if you earn the average returns based on the last 50 years, you’ll end up with a cool $537,628 left over after having paid off the initial $100,000 line of credit balance that you borrowed to begin with! Obviously results will vary and there’s no way to guarantee historical averages will repeat itself, but even if it doesn’t you are still very likely to end up light years ahead of the other option of socking away $300 / month for 25 years.

I can hear the alarm bells going off now. What if mortgage interest rates rise? What if the stock market crashes? Oh my gosh, so much disaster could happen! Well, hold your horses, wait a minute, let’s consider both of these scenarios. Let’s take the worst-case scenario we can think of and assess it’s likelihood. At the same time let’s consider how we could adapt and if we could limit our losses.

What if the stock market crashes 20-30-40% or worse *and* interest rates rise like crazy at the same time?

In order to really assess the risks here, let’s look at what’s happened in the past. The reality is that in the last 42+ years (since 1973) there has only been a single mortgage rate increase that would have warranted a quick reaction. The most significant hike was a 10% rate increase from 10.25% to 20.25% between the years of October 1978 to October 1981 (mortgage rate history); which quickly followed by two years of rapid decline back to 12.5% by October 1983. This is truly a rare event and requires a significant set of circumstances to occur.

Let’s look at how stocks performed during the same time period of the interest rate hike. Between 1978 and 1981 the DJIA increased in value by 25% (stock market history). At any time during the rate increase you could have sold your stocks and put the cash proceeds back against your home equity line of credit, losing very little funds in the process. Alternately, if you were able to weather the expense of the increased mortgage payments of ~$833 / month you would have still earned 25% returns in the stock market during that timeframe; depending if you had $100,000 or an increased value of stocks, your returns would have varied but you would’ve been very unlikely to have lost much, if any at all. Furthermore, the subsequent 3 years in the stock market would have earned you record returns; rewarding you for your long-term view and your resilient approach.

Still there are small odds that the stock market will crash and at the same time the mortgage interests rates rise. As these events transpire there is nothing stopping you from selling your stocks and putting the proceeds back against the mortgage. There is a small chance that you could lose tens of thousands of dollars should this occur, but there is a much, much higher chance that you could earn hundreds of thousands should it not.

What if I have an emergency?

What if I have an emergency and I need access to funds quickly? Where will I get them from? Assuming you don’t have a savings account to cover the emergency cost, you could always sell some of your stock to pay for the emergency. Selling most stocks can usually be done in an hour or two and usable as cash within less than a day.

This decision is a very personal one and isn’t an approach that everyone will be comfortable taking because, like any consideration, it carries both risks and rewards and delving into new territory is a struggle for many. There are many other considerations I didn’t delve into on the topic, but I wanted to provide a high-level for you to think about. Feel free to post your comments, questions or feedback for discussion below.

Brent Mondoux

Founding Partner, Amplified Investments

brent@amplifiedinvestments.com

Investing in real estate